409A to ensure against crazy discounts to employees

company want to grant options to team as low as possible so they can have the benefit from joining

don’t give away the 409A to investors that would screw up the valuation

Valuation = Income / Risk

either decrease risk or increase income

get MOUs

M&A very hard to use to push values. Different acquirers are only able to capitalize assets they are buying to certain extents

Hot air valuations – patent or number of engineers

only useful if it’s stopping a large player from getting to market

need to fight violations to keep patent

Company needs to own patent for it to be valuable for investors

provional patents are a liabilities as they require further resources to be issued

eye balls that cannot be monetized

Not really valuable

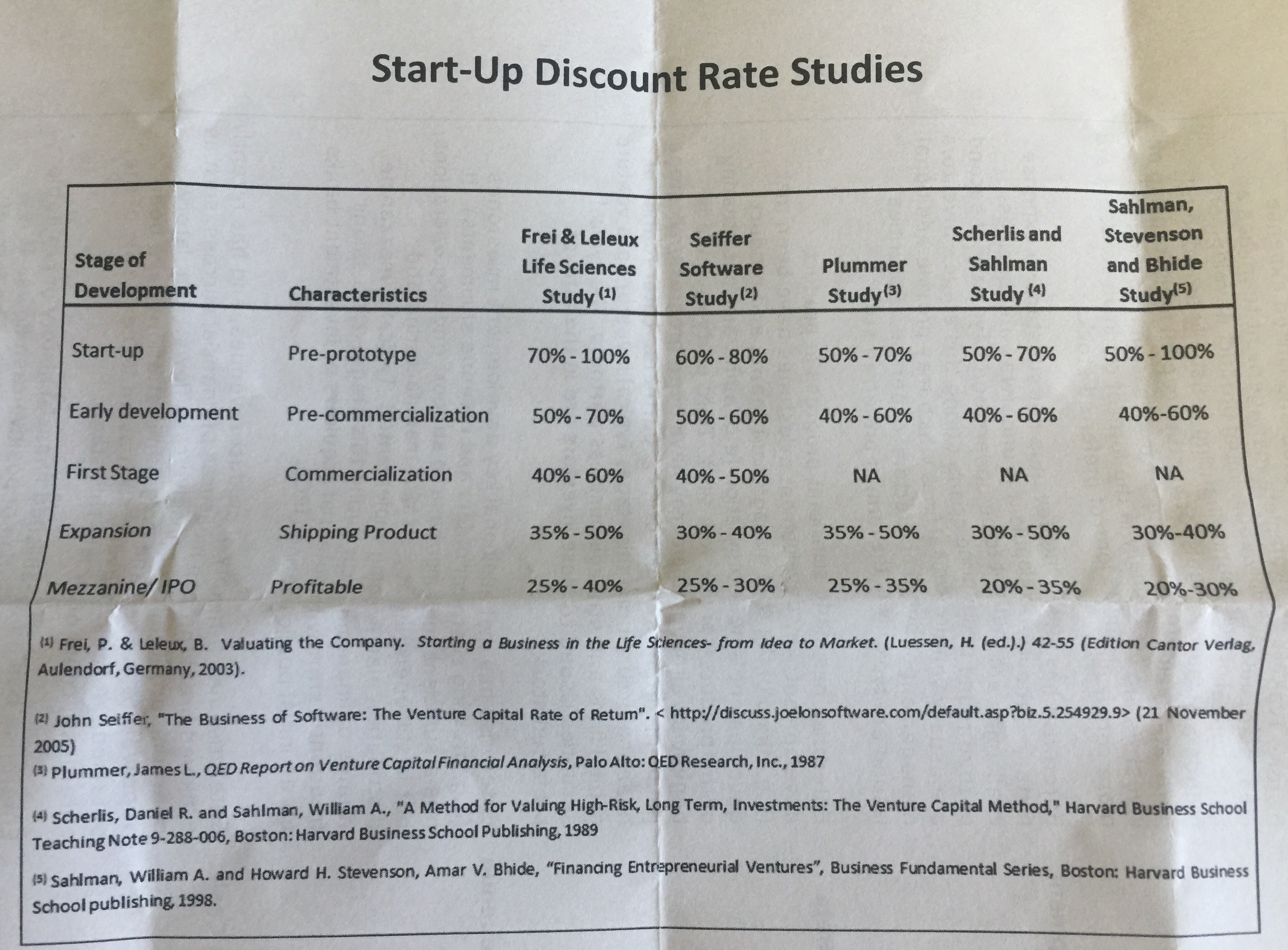

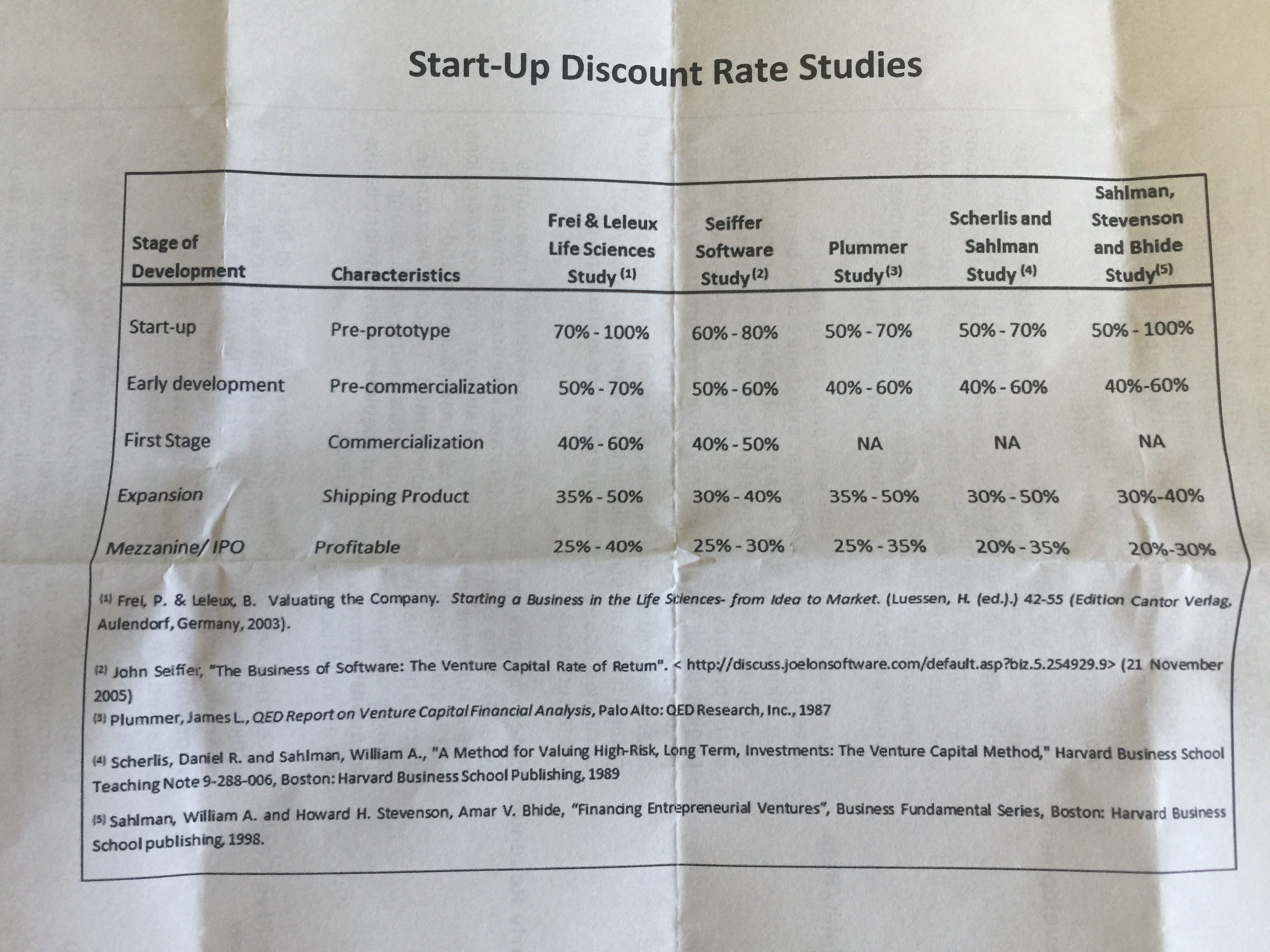

There is a reasonable valuation of projects at different stages

Anything not technology or hardware leads to valuation below 1x of revenue – IOT is hard to value. Is a front loaded hardware play but software play eventually

Towards later stage startups ESOP / Fair market valuation versus investment will converge

convergence is based on successful team execution

Cost Approach to valuation for issuing ESOP

Salary.com useful for making research on cost approach to monetization

expenses incurred since inception

founder salary 60K to 120K per year range

PAR value is meaningless – it’s just a plug number

Post revenue switch to cashflow valuation model

Ensure against red flags in ur cap table

need to have 10-15million shares outstanding

smells and feel like silicon valley

get an attorney who understands Silicon Valley to do it

east coast versus west coast financial instruments they like

Pre-money and Post Money valuations

investors are always thinking of post money

founders are always thinking of pre-money valuation

talk to investors using post money

usually 20% dilution per round

Series C usually leads loss of company control

ventures usually want a bigger chunk when they come in early

need to go after increasing valuation

need to model CAP table before fund raising and share it

Founders who gave up too much equity early on makes the company unfundable

Funds older than 5 year old they can’t fund new ones

Each fund last for 10 years

VCs need to raise more funds to invest

Watch out for

investors want to be able to convert to common shares results in Full participating

watch out for liquidation preferences – 2X or 3x

lesser participation more aligns the investors with founders

full participating investors will want to exit earlier versus founders

VC method

Comps / Peer group’s revenue multiple to get valuation – need to spend a lot of time to build peer groups and prove the peer group multiplies

social media valuation is slowly coming down

which year become profitable = when most likely to exit

they apply valuation of earliest most likely to exit by 50% discount and then apply risk discount

in the valley they only care about revenue growth and not income

SAAS don’t make money they are putting money back in the business

Revenue todos

don’t use top down revenue projections

use bottom up revenue projections

Need to see where the holes are and try to break it. Need to ensure the valuation is defendable

projectiond keep rolling down as time passes along and things start playing out