2020 Corona virus sell offs

May 2019 US China trade war sell off

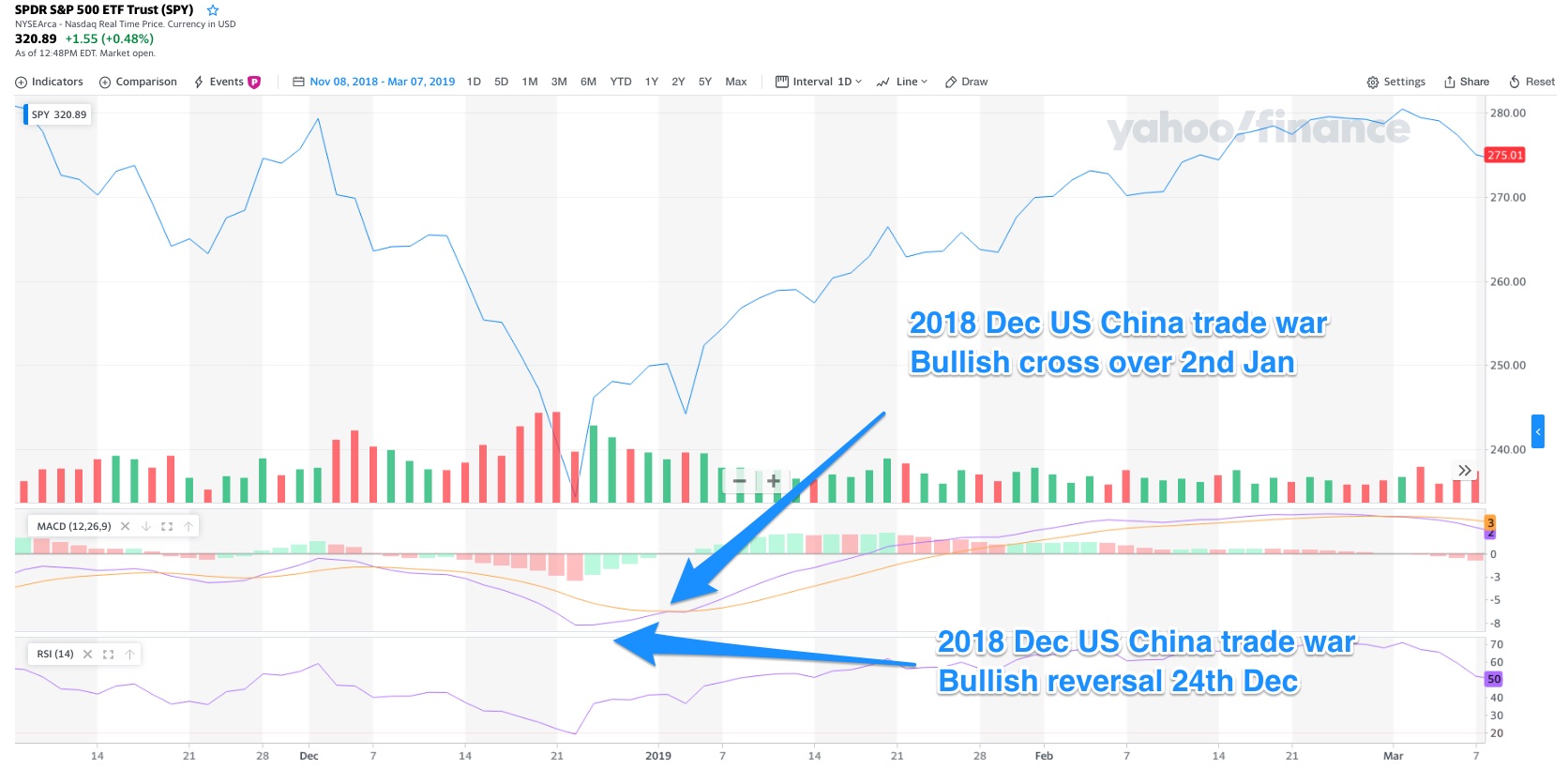

Dec 2018 US China trade war sell off

2003 Sars sell offs

2001 September 11 World trade center collapse

2008 Financial crisis

notes, learnings and reflections for future self reference

2020 Corona virus sell offs

May 2019 US China trade war sell off

Dec 2018 US China trade war sell off

2003 Sars sell offs

2001 September 11 World trade center collapse

2008 Financial crisis

Crash happened when too high a percentage of borrowers in the system are Ponzi borrowers.

https://en.m.wikipedia.org/wiki/Hyman_Minsky

Good news reporting should seeks to inform rather than sensationalize with attention grabbing headlines. Its easy to appear data driven but still be misleading if you do not use the proper frame for understanding the numbers

When on the receiving end of predictions made by external parties it is important to understand the underlying agenda they are trying to achieve. When examined thoroughly, predictions made by investment banks are so bad and contradictory, they should just stop making public declarations.

However if taking into account their objective is not to inform but to incite a trading decision by their clients so as to make a commission or offload losing positions on their trading books, it makes perfect sense.